EA at a Glance

EA Games (EA) is a multinational software company that designs standalone and franchise video games for a multitude of different hardware devices. The company runs a multitude of different franchises within the gaming space, including Battlefield, the Sims, Fifa, and Madden, just to name a few. Devices this software is designed for range across mobile, Xbox, PC, PlayStation, and other major gaming consoles.

(Source: EA Games 1Q2018 Earnings Call Slides)

(Source: EA Games 1Q2018 Earnings Call Slides)

EA is generally coming out of a period of evolution and changes within the gaming industry. Over recent years, the industry has been fundamentally moved by the two major trends of the death of retail and the exponential growth of the cloud. This has allowed software companies to reallocate all of their services to download licensing and other non-physical delivery of products to ultimate end users. At the same time, this has also led to a general widening of margins for many companies within the space, as packaging design and other expenses have been taken out of the equation.

These changes have also led to another industry-wide trend in the software space, namely what is referred to as software as a service (SaaS). This premise encompasses the idea that software products are provided as a service through the cloud and hosted on company-owned servers and accessible from multiple devices through the internet. This is in contrast to the previous decade involving local installation of software on one's computer or device.

This idea of SaaS provides software producers with a major advantage however in that they are now able to actively update files and add content on a rolling basis. The games which used to be standalone titles with very distinct iterations have grown into moreso living games which have full content updates and additions that are much more expansive than simple patches. This provides producers with a key advantage in that, under this model, they can sustain a user base on an individual title by providing constant engagement and updates to keep users from getting bored and moving to other games. Rather than being forced to create an entirely new entity of a game and throw an arbitrary number at the end of the title, the individual entities have much longer lives. This ultimately allows producers to save costs through not needing to create an entirely new standalone title. Furthermore, users feel more engaged as a result, due to both the constant content updates and also the sense of community that each game in and of itself facilitates.

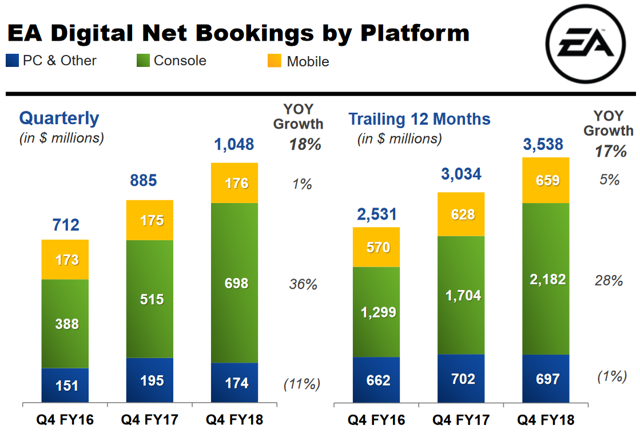

This trend can be seen substantially in the recent growth of the company's revenues, which are seeing explosive growth through digital platforms relative to traditional delivery methods.

(Source: EA Games 1Q2019 Earnings Call)

(Source: EA Games 1Q2019 Earnings Call)

The Gaming Revolution of 2017/2018

2017 and 2018 ultimately represented a major shifting point in the mainstream presence of the gaming industry. While many people will simply refer to Fortnite as being the catalyst for this widespread acceptance, it was simply the last in a series of games that allowed the industry to reach the critical mass necessary to reach the mainstream.

What has ultimately led to the rise of gaming over recent years is the enhanced prevalence of esports being taken seriously, with substantial prize pools and competitive followings growing to the level of almost professional sports. One can see the substantial, multimillion prize pools that exist for top players in the spaces. Competitive games such as Dota 2, League of Legends, Overwatch, and others have cultivated massive followings, with League of Legends experiencing more than 100 MM live viewers for top-level tournaments.

This is similarly the case with EA in that they host competitive games such as Madden, Fifa, and other sports titles which have substantial prize support and competitive infrastructure in-place to keep the titles relevant for years to come. Furthermore, the company's virtual monopoly on the sports franchises creates a massive competitive moat for it that many of its peers' premier franchises lack. The battle royale and MOBA content seen over recent years has reached overly competitive levels, with borderline copies of games being released by other studios with blatant disregard for IP, especially in China and international markets. EA, however, due to their decision to retain focus on their key franchises, have faced much less impending competition as a result.

Furthermore, EA represents one of the few companies that continues to develop standalone titles in a more aggressive manner with a goal of ultimately adding them to their core portfolio. For instance, upcoming game Anthem is being hyped up as an incredibly developed game that will be a core EA franchise for years to come.

Impending Shift to Subscription Model Extremely Likely

A massive decision undertaken by the company recently is the test drive of a subscription service for PC content. This marks a major evolution of the gaming industry as typically the industry is incredibly seasonal. New titles hit the market in late fall and early winter to coincide with cold weather and generally more electronic device use, and producers hope to reap as much profit as possible in the initial period after release. The subscription model on the other hand solves this key issue of seasonality, and what has historically been volatility in revenue for these content producers.

While this is currently only set for use on the company's PC content, rhetoric put out by the company during its last earnings call leads us to believe this is moreso a markets test that will lead to a full company rollout across all consoles in the future.

Fiscal 2018 was a record year for Electronic Arts as measured against almost every major financial metric, from revenue to operating income to cash flow. Our success is driven by the way we have changed and continue to change our relationship with players. They want more depth in their favorite games and fresh content that can hold their attention year-round.

As a result, we've gone from one-off interactions at a moment in time to ongoing engagements with consistently changing dynamic worlds. It's a situation analogous to the transition we've seen in the software-as-a-service industry. Consequently, our business already looks very SaaS-like, with live services and subscription making up a greater and greater portion of our revenue. This has made our business much more stable and enabled us to deliver a dependable and growing cash flow to investors.

-Blake Jorgensen, CFO

(Source: EA Games 1Q2019 Earnings Call Prepared Remarks)

The company appears to have fully embraced this idea, as this was reiterated time and time again on the call when addressing analysts during Q&A.

So let me grab the first one. At its very core, you've heard us talk a lot about subscription plus cloud gaming and the opportunity for those two things to fundamentally disrupt the way people access and enjoy games like nothing before, much in the same way as it's disrupted enjoyment and engagement in movies and music.

And so we've talked about a three to five-year time horizon. We believe that cloud gaming is going to make a meaningful contribution to the way players engage with games. And of course, what that does mean is it really doesn't matter what device you're accessing it by. The experience that you have is governed by the size of the screen and the amount of time you have to play

And so everything we're building right now, we are thinking about a world where we will not be bound by device. We will not be bound by local compute or memory, but much of these experiences will exist in the cloud, and you'll access them based on whatever device you have access to at the time.

-Andrew Wilson, CEO

(Source: EA Games 1Q2019 Earnings Call Q&A)

Ultimately, this seems like a no brainer for the company. Current pricing plans are for $15 per month or $100 per year on the PC subscription service. Most of the major concern regarding this model lies with the boom factor that many releases have. If subscribers have access to these upon release, this could impact ultimate new game sales. However, as the exact structure hasn't been finalized and is still in the beta-testing phase with the market, these quirks will be refined. There's the possibility for things like "Early access" to new releases for some amount with the first 6 months post-release being a free access blackout period. The way the company could monetize this concept is endless while still taking in the monthly premiums from subscribers.

Increased Monetization of All Titles Drives Growth

Furthermore, through giving subscribers access to a multitude of older titles, it allows them to stick their hands into a multitude of games. This ultimately leads to more micro-transactions for in-game content which will be a major driver of producers' revenues moving forward. While EA received substantial backlash for the Star Wars loot box fiasco, which was essentially a pay-to-win monetization, the shift to making in-game purchased content primarily aesthetic and has minimal implications on actual gameplay has received absolutely zero backlash. On top of this, in a game where everyone's avatar is generally fairly generic, the ability to customize appearances is an extremely sought after and enjoyed experience for users.

Not only that, but shifting to a subscription service could allow for account-wide transactions, with single items being purchased in microtransactions being able to be applied retrospectively across all games. For instance, say purchasing your favorite World Cup teams jersey and having some form of it be equipped aesthetically for all multiplayer games from Sims to Fifa to Battlefield. This would not only create more value for consumers as they wouldn't have to worry about their purchases being useless if they stopped playing a single game, but it would also allow substantially more marketing of events to all users across the company's entire gamer base.

Buyback Program Supports Shareholders

Another attractive facet of EA's current management plan is its unique approach to returning value to shareholders. While many companies traditionally supply a quarterly dividend, EA opts to rather use substantial share buybacks when free cash flow permits. This creates an extremely flexible capital budgeting methodology for management, so if the company sees attractive investments in new content through either development or acquisition, cash can be diverted from expanded buybacks to these capital growth opportunities, which will ultimately drive further unlocking of value. Meanwhile, if buybacks are not extended, there will likely be no share-price impact relative to if this were a dividend cut, as the buyback programs are detailed in their entirety and must be extended or reinstated after their initial planned ending. This idea of capital flexibility was furthermore touched upon in the company's recent earnings call.

I'll hit that first. It's all three of those things. As Andrew mentioned, running a broad subscription service requires great content. And so we're always looking for great content and really great studios that can build that content. We partnered with Respawn for some time to get to know them. We believe they're a studio that can build not just the great games they're building today, but great games for a long time to come. And so it's a great studio and great partners that we can bring to the table in both mobile and console and PC, but also technology that will help us either in subscriptions or streaming, and you'll probably see some of that stuff to come.

Most of it is probably more small to midsized than large just because there's not that many large companies out there, but we'll look at everything, and we want to maintain that flexibility. And that was really the primary reason for not doing a dividend is that we felt if we started a dividend it would be much harder to stop it if there was some reason to flex up to do something larger. And that's the reason we decided to stay with the buyback. We feel it's the most efficient way to do it and it gives you full flexibility going forward.

- Blake Jorgensen, CFO

Additionally, looking at the company's current buybacks, they were most recently doubled to $2.4 bn for the next two years. Furthermore, the company has over $4 bn in free cash on its balance sheet currently set for no defined use. It is likely that as momentum in the gaming industry continues over the coming years, a further acceleration of buybacks per year from the current $1.20 bn per year is virtually guaranteed barring an industry-wide collapse in popularity.

Projections and Valuation

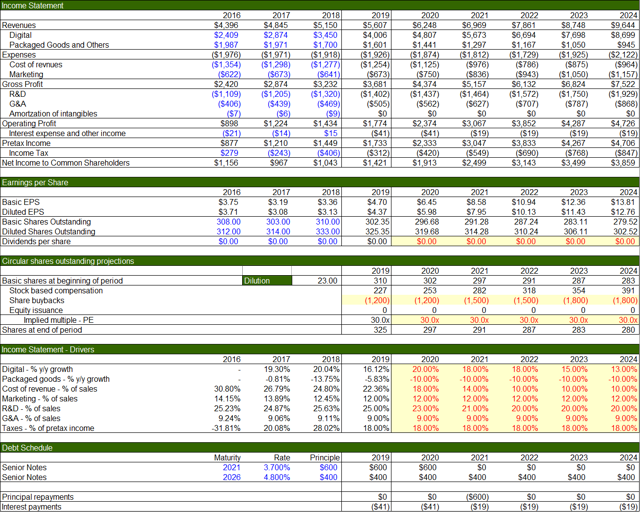

For our analysis of EA Games, we built out a revenue build and income statement and valued the company on both a multiples basis and a DCF basis using an exit multiple and perpetuity growth rate. Looking first at our revenue build assumptions below:

(Source: Self-made Model; Historicals from Company Filings; Some numbers backed into based on audited and unaudited Company reported numbers)

(Source: Self-made Model; Historicals from Company Filings; Some numbers backed into based on audited and unaudited Company reported numbers)

Major assumptions of note are the revenue growth rates and the substantial declines through time of cost of revenues and R&D. Furthermore, we also assumed a fairly large buyback level; however, these buybacks are all substantially within free cash flow while leaving an excess cushion, so we find them to be relatively likely given our other assumptions. The substantial decline in cost of revenue as a percentage of sales is driven by the company's increasing emphasis on developing live content and the planned shift to subscription services. We reduced this through time as the subscription model shift and increasing player base should keep these costs fairly fixed to declining through time. Even looking at the company's implied definition of this line item, one can see the extreme likelihood of margins continuing to expand against this backdrop:

Cost of product revenue consists of (1) manufacturing royalties, net of volume discounts and other vendor reimbursements, (2) certain royalty expenses for celebrities, professional sports leagues, movie studios and other organizations, and independent software developers, (3) inventory costs, (4) expenses for defective products, (5) write-offs of post launch prepaid royalty costs and losses on previously unrecognized licensed intellectual property commitments, (6) amortization of certain intangible assets, (7) personnel-related costs, and (8) warehousing and distribution costs. We generally recognize volume discounts when they are earned from the manufacturer (typically in connection with the achievement of unit-based milestones); whereas other vendor reimbursements are generally recognized as the related revenue is recognized.

(Source: EA Games 2019 10-K)

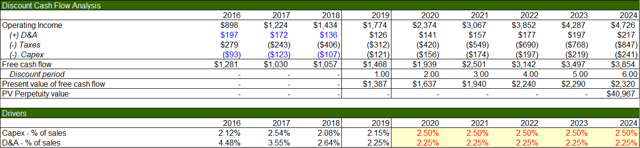

Looking at our free cash flow projections below, this leads to the following basic DCF buildout. Please note we did not project out working capital due to the extremely low working capital needs inherent in the company's business model:

(Source: Self-made Model; Historicals from Company Filings; Some numbers backed into based on audited and unaudited Company reported numbers)

(Source: Self-made Model; Historicals from Company Filings; Some numbers backed into based on audited and unaudited Company reported numbers)

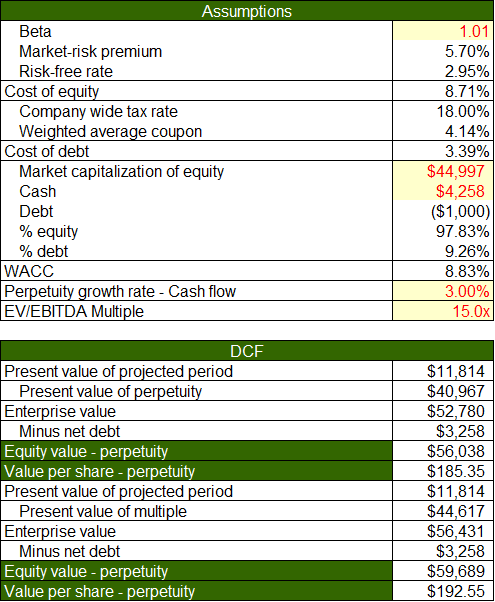

This then leads to our WACC build (note we used weighted average coupon versus YTM for COD due to not having access to secondary market debt pricing at this time) and ultimate DCF valuations:

(Source: Self-made Model; Historicals from Company Filings; Markets based numbers from Yahoo Finance)

(Source: Self-made Model; Historicals from Company Filings; Markets based numbers from Yahoo Finance)

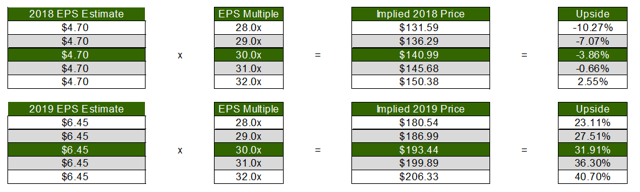

Contrasting this to our PE valuation below:

(Source: Self-made Model)

(Source: Self-made Model)

As one can see, based on our assumptions, there appears to be another 30-40% upside in the company's stock price from current levels. Given the relative momentum and favor of tech right now, alongside the positive earnings growth story that will likely continue to play out through 3Q2018, we feel comfortable taking exposure to EA even after the recent trade up. We primarily attribute the undervaluation to the recent decision to begin the slow transition to a subscriber model, but ultimately will likely see multiple expansion for the company similar to, though likely not to the same extreme extent as, Netflix (NASDAQ:NFLX). As increased clarity and guidance is given on the business model shift, in addition to increasingly successful monetization efforts of microtransaction content, we expect the price to rapidly converge with the upside presented here.

Risks

The largest risk with regards to EA is the risk of failure in the business model shift to a subscription-driven service. If the company makes any errors to create a lack of trust or favorability for EA relative to peers with this model, the company would likely face substantial PR backlash or poor market performance of the service. We see this as a tail risk. However, it is a fairly substantial tail risk, and thus the company's decisions as this shift is rolled out will be analyzed extensively, and if any negative sentiment begins to materialize, a sale of the stock would be warranted.

Another risk associated with the company is if the recent video game fanaticism is simply a fad rather than a larger consumer trend within the space, top-line revenue growth numbers will likely be less than we have predicted, with margins widening at a slower pace than we predict. This is a risk. However, given the extensive growth of esports over recent years, we also view this risk as very unlikely.

Conclusion

Overall, we view EA as our top pick within the gaming software peer group, as the company's competitive moat with such standalone franchises as Battlefield, Fifa, Madden, and Anthem prevent the market share wars many peers in the MOBA and battle royale style offerings currently face. We further view the company's decision to begin developing a more rigorous subscription model as a key driver within the space, as EAs offering of titles is substantially more supportive of this relative to its peers which focus more on the esports and competitive gaming revenue streams. Finally, with substantial share buybacks for the near future, likely to be expanded into the future, there will be continued support of the share price by management as excess cash is returned to shareholders.

Overall, we view EA Games as our top video game stock and continue to hold our position into the immediate future barring a material change in fundamentals or market trends.

Disclosure: I am/we are long EA.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.